IAMGOLD Announces First Gold Pour at Côté Gold

IAMGOLD, a portfolio company in RCF VII, has announced a first pour at its Ontario gold mine

IAMGOLD, a portfolio company in RCF VII, has announced a first pour at its Ontario gold mine

Announcement: Anna Shave Has Joined the Team

RCF Innovation II portfolio company Mevco is adding Rivian’s R1T to its electric vehicle fleet

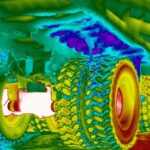

Andrew Jessett provides an investment update on mining innovation firm Pitcrew AI

Leichhardt Industrials, a portfolio company in RCF Opportunities Fund L.P., set to acquire Lake MacLeod’s assets from Rio Tinto’s Dampier Salt

RCF Innovation II has invested in Pitcrew AI which provides automated tire inspection to help mines enhance safety, increase efficiency, and reduce environmental impacts

Phibion, a portfolio company in RCF Innovation I, won the 2023 Premier of Queensland Export Award, winning the Resources & Energy category

Brett Beatty, Partner, Investment Team Leader discusses zinc, copper, and vanadium outlooks with S&P Global